Every couple of decades, a game-changing technology emerges that triggers a wave of innovations. Known as “general purpose technologies” by economists, they represent a major new enabling technology that has wide application across many use cases, deliver profound impact, generate substantial value across the economy, and ultimately affect all industries. Artificial intelligence, known as AI, is one such technology.

We sat down with Tom Ricketts, Evolutionary Tree’s CIO and Portfolio Manager to discuss the implications of AI for investors and portfolio holdings. An excerpt of our conversation follows.

Is AI finally going mainstream?

Tom: Very much so. After decades of behind-the-scenes development, AI has passed key thresholds for technical and economic feasibility that we believe will drive growth in AI-related services, software, and data businesses. As you know, we are fervently “anti-hype” in our approach, so we pay attention to where new technologies reside on what we call the hype-readiness continuum. What’s so exciting is that AI really is going mainstream, and thus investors should take notice.

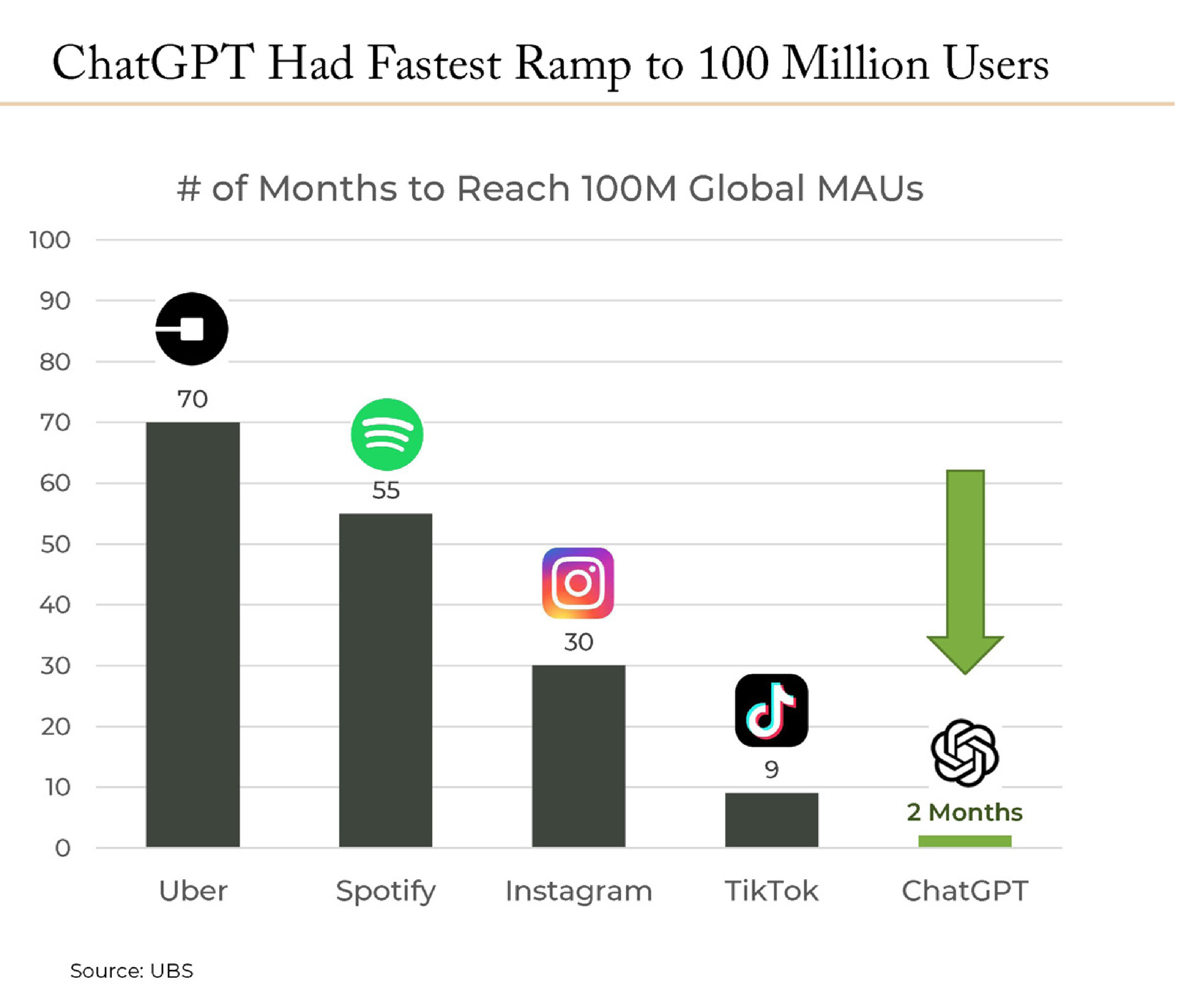

In fact, this wave is happening even faster than the adoption of the personal computer, smartphones, and many popular apps. Take ChatGPT, for example. The chatbot from OpenAI and its partner Microsoft reached 100 million active monthly users just two months after launching. Some analysts are hailing ChatGPT as the fastest-growing consumer internet app in history. By comparison, it took social networking app Instagram 30 months to ramp up to 100 million users.

We believe AI has moved beyond the hype phase and has real utility and implications that are pretty far-reaching—of a magnitude in importance similar to that of the invention of the computer or the Internet.

What does the widespread adoption of AI mean for investors?

Tom: As investors who prioritize innovation-driven growth equities, one of the things we’re most excited about is the potential for AI adoption to catalyze growth in the tech sector as a whole, and consequently, for growth stocks. Think about how powerful it was for the tech sector when the personal computer was launched, spawning global adoption of not only personal computers, but also servers, software applications, and IT services. That’s the thing about general purpose technology-driven waves: They create opportunities to launch new services and enhance existing products. And while the adoption of AI has really taken off, we believe broad and deep utilization of this technology is still in its early stages, holding immense potential for the tech sector.

We believe the widespread adoption of AI will also dramatically enhance existing software suites and platforms, as leading tech companies add AI functionality to boost productivity, apply data, and generate new content. This is profound, especially when you consider that enterprise software stocks have been out of favor for well over a year. As investors begin to appreciate that enterprise software benefits from AI, they’re likely to reassess their stance on these businesses and stocks. And, given these companies’ relatively low valuations, in our opinion, they may begin to re-embrace them. Of course, not every software company will benefit. Only those that integrate AI in ways that bring tangible value to users will benefit. We believe that AI will create opportunities for the leading software suites, as these platforms may be the best way to “distribute” AI functionality to end-users.

The third implication is that AI is likely to accelerate ongoing evolutionary shifts within the technology landscape, including the transition to cloud computing and the adoption of modern data platforms. This is primarily due to the fact that companies can’t harness the full potential of AI without accessing and pooling a critical input: data. And the best way to break the silos of traditional data centers and on-premise software is to move these applications and associated data into the cloud. Once there, it becomes vastly easier to use this data to apply machine learning and AI to create algorithms and generate insights and productivity improvements.

What does the AI tech stack look like?

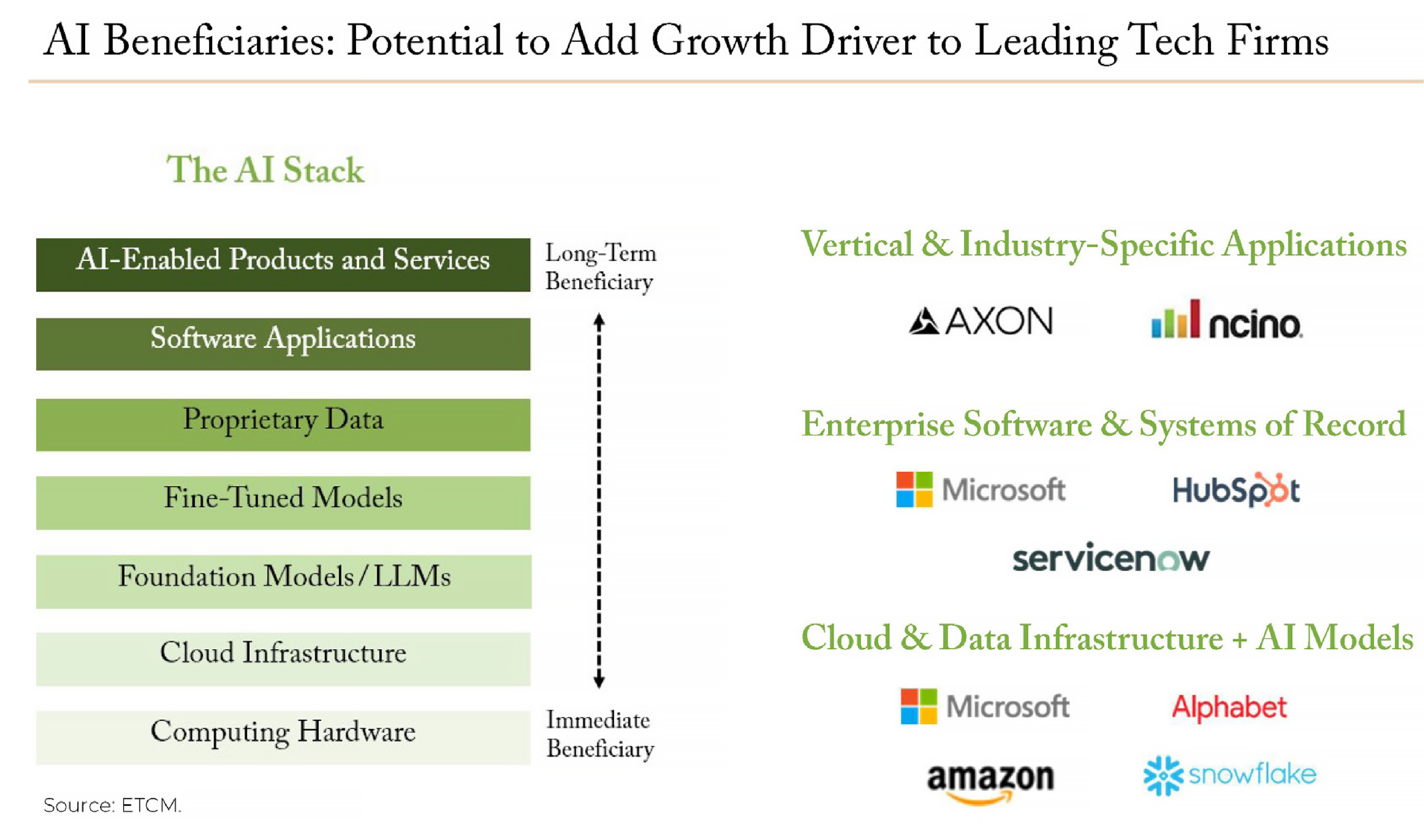

Tom: The AI stack is made up of different building blocks. At the bottom, we have the powerful AI accelerators and supercomputers that do the heavy computing work. Moving up, we find the cloud infrastructure that allows data to be trained on foundation models, refining them into more specialized models for specific applications. As we climb higher, it’s exciting to imagine that most software applications will add AI functionality. And ultimately, over the coming years and decades, we will see a growing number of AI-enabled products and services across the economy.

In the illustration below, we show several portfolio holdings that we think could benefit from the application of AI in the long run. We’re already witnessing a surge in demand for machine learning and AI modeling services offered by cloud infrastructure giants like Microsoft Azure, Google Cloud, and Amazon’s AWS. Not only that, but we’re also seeing enterprise software companies like HubSpot and ServiceNow roll out AI-related functionality, such as HubSpot’s “ChatSpot,” which assists salespeople in creating engaging content for emails or blog posts. Longer-term, it seems reasonable to believe that vertical or industry-specific software providers—especially those with large and proprietary datasets—will find innovative ways to leverage AI. Take companies like Axon and nCino, for instance. Axon can utilize video and evidence data to inform its AI models for law enforcement customers, while nCino can dig into its data to analyze borrowers and loan performance for banking customers. The bottom line is that AI is likely to spur many new AI services that can sustain growth for enterprise software companies. We’re confident that our portfolio is well-positioned to benefit from AI opportunities over time.

Who is positioned to lead the AI innovation wave—any companies we could dig into further?

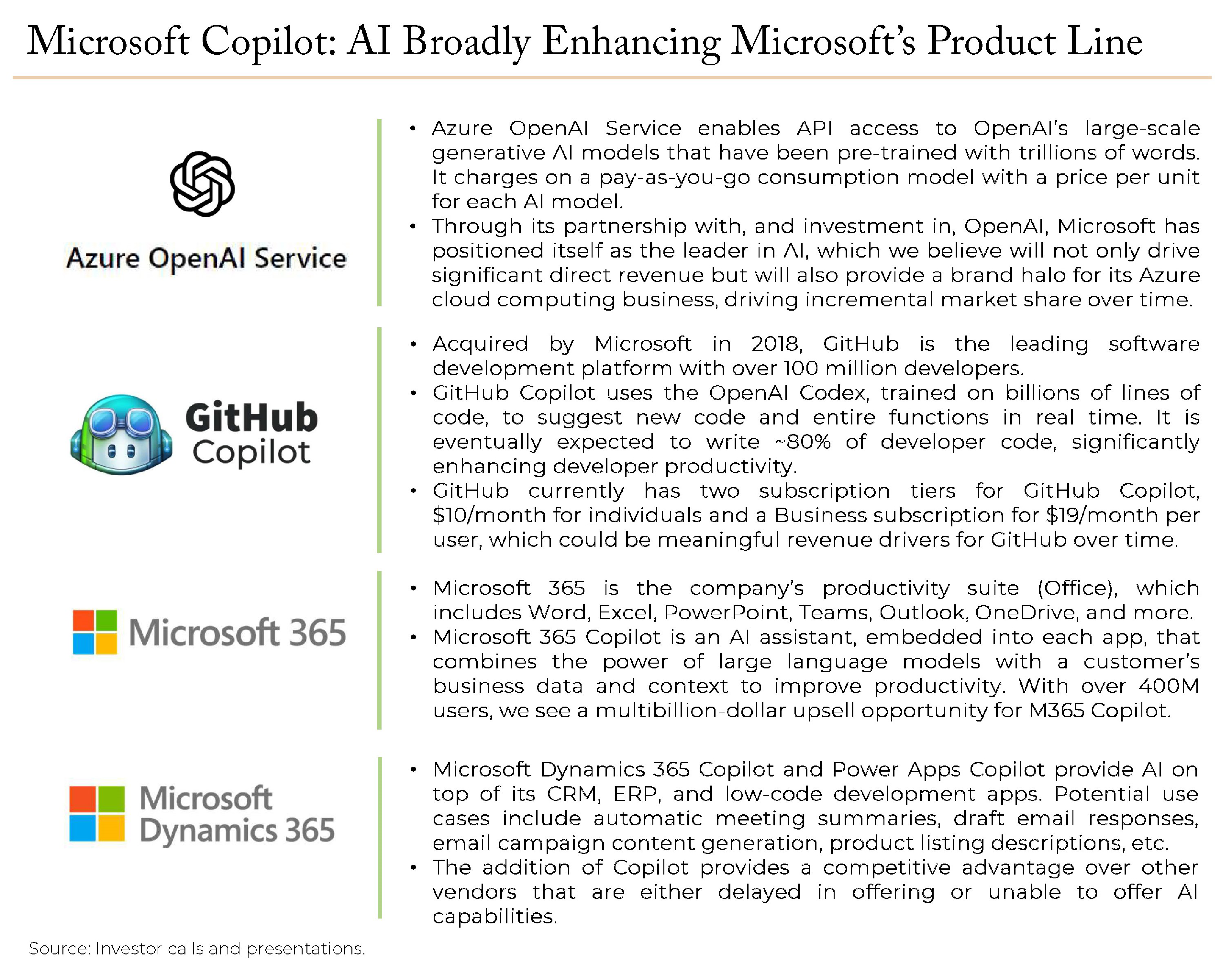

Tom: No company demonstrates the implications and potential of AI better than Microsoft, currently our largest holding, which we believe is the standout leader in the commercialization of AI. As we showcase below, Microsoft is in the process of reinventing almost its entire line of products and services using AI. Microsoft has coined the marketing phrase “Copilots” to describe how AI can benefit users of its software.

The idea is that AI can function as an assistant, or copilot, when you are using any of its products. For example, software programmers that use Microsoft’s GitHub platform for creating and storing software code can also use the GitHub Copilot, which uses generative AI to actually write code (yes, automatically) in response to natural language queries or as auto-fill. Microsoft, along with its partner OpenAI, is also applying ChatGPT to offer assistance in various applications, such as search or in its Office suite. Furthermore, Microsoft offers the powerful OpenAI large language models (LLM) that power ChatGPT to enterprise customers through its Azure OpenAI service.

We believe that AI will substantially enhance Microsoft’s product line, arming the company to drive deeper adoption of higher-tier offerings and to create new service lines to sustain growth. Just as cloud computing rejuvenated Microsoft’s business (notably Azure and Office 365) over the past five-plus years, we see AI adding another wave of growth.

Disclosure: This is not a recommendation to buy or sell any security. There is no assurance that the portfolio will continue to hold the same positions in the companies described. Portfolio positions may change at any time. Data or information communicated based on information from third parties is believed to be accurate, but no representation is made that the information provided is correct and complete. All data is subject to change. Company logos and website images are used for illustrative purposes only and were obtained directly from the company websites. Company logos and website images are trademarks or registered trademarks of their respective owners and use of a logo does not imply any connection between Evolutionary Tree and the company.