Evolutionary Investing is an investment approach that takes advantage of an evolving economy.

This unique approach positions investors to benefit from leading innovators driving structural or evolutionary shifts across a growing number of industries, while seeking to minimize the negative impacts of disruption. We believe this is the next generation of concentrated growth investing.

We live in the Age of Innovation where the pace of innovation is accelerating. Innovation is now the primary driver of value creation and should be a core part of every investor’s allocation.

While innovation is widely viewed as important, we believe the power of innovation is now paramount. Innovation has become the primary driver of value and wealth creation across the economy. Reflecting this dynamic, the economy is shifting from an industrial-era, tangibles-based economy to one dominated by intangibles—in essence, by the power of ideas.

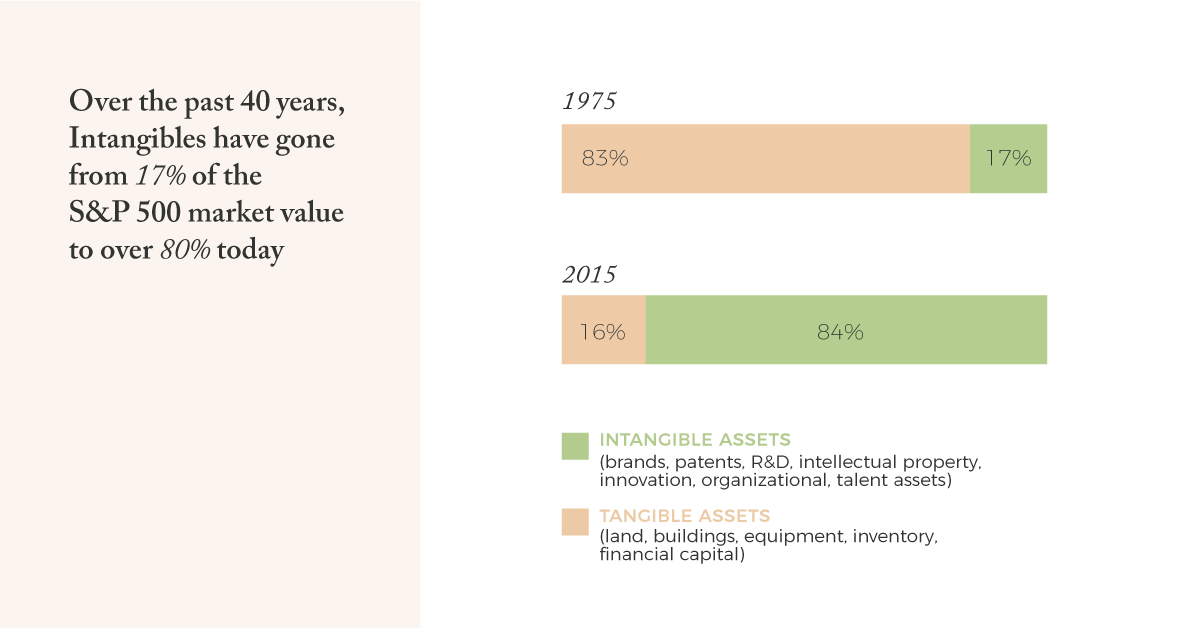

The evidence is clear. In the 1980s, tangible-based assets (capital, buildings, equipment, etc.) made up about 70% of the market value of the S&P 500, with intangibles only 30% of the value. Over time, these drivers have flipped, with intangibles or intellectual capital (brands, IP/patents, innovation, talent, etc.) now comprising over 80% of the value of the S&P 500, while the tangibles-based economy is now less than 20% and shrinking. Ideas and innovation are now the primary creators of wealth today.

The rise of Internet-based technologies, cloud computing, mobile applications, and other “digital building blocks” are increasingly integrated into more and more products and services, accelerating innovation cycles and the shift to next-generation business models and offerings.

This never-ending series of new innovations is driving the evolution of business models and industries, and, in the process, creating new winners and losers.

In decades past, innovations arose at a slower pace and were absorbed by incumbents with less disruption. Today, with accelerating change, new innovations can drive profound structural changes within and across industries—creating both long-term growth opportunities for leading innovators and risk to those firms failing to adapt. The days of graceful maturity for incumbents has given way to next-generation products or services displacing less-innovative offerings. Shifts from the old generation to the next generation are now happening more rapidly. We call these evolutionary shifts, and they can offer both opportunity and risk for investors. Examples of evolutionary shifts can be found in most industries and include: the shift from traditional media to video streaming, from on-premise client-server computing architecture to cloud computing and software-as-a-service, and from traditional retail to e-commerce.

Regardless of one’s view on the debate between growth and value, investors today are struggling to keep pace with these changes, driving the need for an updated investment approach focused on innovation.

Many value investors may struggle with moving beyond tangible assets as a primary driver and with embracing innovative companies in industries outside of their core competence. At the same time, some growth investors tend to only search for growth for growth’s sake, and can be late to embracing new innovations until they have already scaled up in the marketplace. The common issue is that both traditional approaches tend to rely heavily on conventional backward-looking metrics, as opposed to understanding the long-term qualitative and strategic drivers that determine the future path of growth.

Growth is an outcome, not the driver. Innovation and evolutionary shifts are root causes of growth.

At Evolutionary Tree we are exclusively focused on identifying what we believe are the root causes of future growth for companies and industries—innovation, evolutionary shifts, and secular trends.

Many traditional investment managers, including index funds, tend to over-diversify, diluting the power of those rare innovators that drive much of the value creation. In the Age of Innovation, we are increasingly witnessing leading innovative companies capturing a growing percentage of profits within each industry, the “winner takes most” dynamic that is more prevalent than ever. We believe a concentrated approach—through owning a select group of leading innovators—is necessary to optimally benefit from investing in innovation and evolutionary shifts.

These trends drive the need for an updated investment approach, which we call Evolutionary Investing:

- Focus on identifying important innovations and leading innovators pioneering them.

- Understand how these innovations drive secular trends and evolutionary shifts over time.

- Tap into a dedicated research effort that systematically tracks innovation, innovators, and secular trends.

- Benefit by owning innovation-focused, concentrated portfolios of leading innovators benefiting from evolutionary shifts and secular trends.

Bottom-line for investors: We live in the Age of Innovation and this changes how you should invest.

Investment strategies must adapt to a world of continuous—and accelerating—change, positioning investors to benefit from next-generation products and services, while avoiding firms being hurt. The new investment objective is to navigate these changes for the long-term benefit of clients.

Evolutionary Tree pursues this objective by building innovation-focused, concentrated-growth portfolios of leading innovators that, we believe, are positioned to add value for clients over the long term. With an Evolutionary Investing approach to investing, we help clients lean into the future and not on the past.